Retirement is not the end of your financial journey — it’s the beginning of a new chapter where stability, security, and sustainable income take center stage. One of the most effective ways to achieve this financial balance is through hybrid and balanced mutual funds. These funds offer a smart blend of growth and protection, which is exactly what retirees need in today’s unpredictable financial environment.

What Are Hybrid and Balanced Mutual Funds?

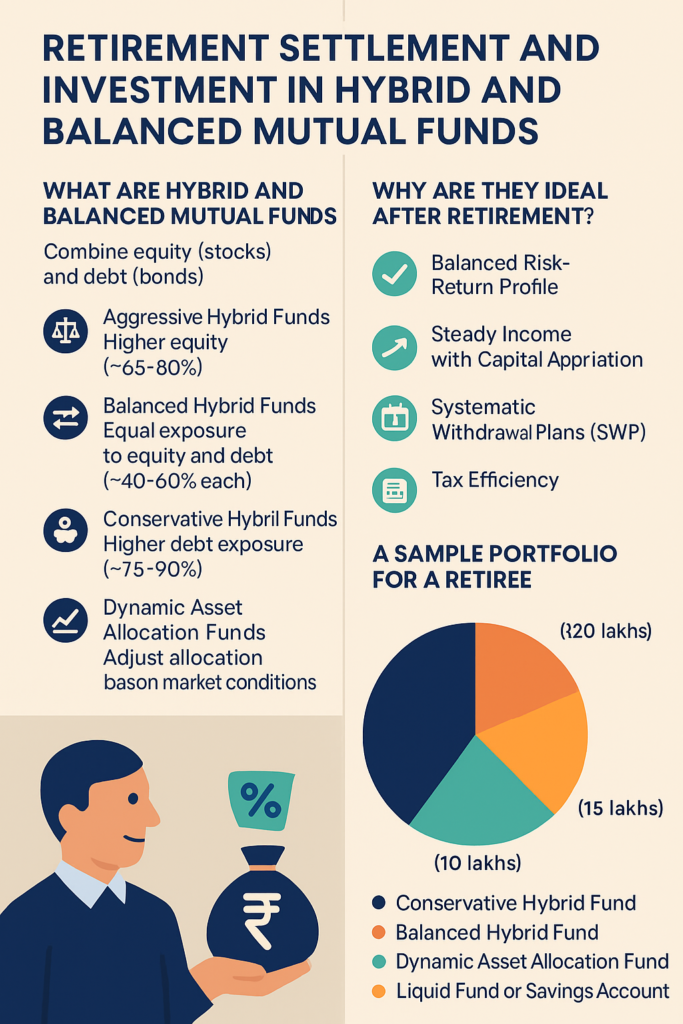

Hybrid mutual funds are investment vehicles that combine equity (stocks) and debt (bonds) instruments in a single portfolio. Their goal is to offer the best of both worlds — growth from equities and stability from debt.

There are several types:

- Aggressive Hybrid Funds: Higher equity exposure (~65–80%)

- Balanced Hybrid Funds: Equal exposure to equity and debt (~40–60% each)

- Conservative Hybrid Funds: Higher debt exposure (~75–90%)

- Dynamic Asset Allocation Funds: Adjust allocation between equity and debt based on market conditions

Why Are They Ideal After Retirement?

1. Balanced Risk-Return Profile

Hybrid funds are designed to reduce the extreme volatility of pure equity funds while providing better returns than traditional debt instruments like fixed deposits or savings accounts.

2.Steady Income with Capital Appreciation

Debt components generate regular income, while equity investments offer long-term growth. This combination ensures your corpus doesn’t just sit idle — it works for you.

3. Systematic Withdrawal Plans (SWP)

With SWPs, retirees can withdraw a fixed amount regularly while the remaining corpus continues to grow. This offers predictability in cash flows and preserves the capital base.

4. Tax Efficiency

Long-term capital gains from equity (over ₹1 lakh) are taxed at 10%, and those from debt funds are taxed based on your income slab. With proper planning, hybrid funds can be more tax-efficient than fixed deposits or annuities.

Real-Life Strategy: A Sample Portfolio for a Retiree

Let’s say you’ve retired at 60 with ₹50 lakhs to invest. Here’s how you might allocate:

- ₹20 lakhs → Conservative Hybrid Fund (steady income)

- ₹15 lakhs → Balanced Hybrid Fund (moderate growth)

- ₹10 lakhs → Dynamic Asset Allocation Fund (market-timed exposure)

- ₹5 lakhs → Liquid Fund or Savings Account (emergency reserve)

This diversified approach ensures liquidity, risk management, and long-term growth.

Points to Keep in Mind

- Choose funds with a proven track record and consistent performance.

- Look at the fund manager’s experience and the AMC’s (Asset Management Company) reputation.

- Review your portfolio annually to rebalance or adjust based on income needs and market conditions.

- Avoid putting all your money in aggressive hybrids unless your risk appetite is high

Final Thoughts

Retirement doesn’t mean pulling out of the markets — it means investing smarter. Hybrid and balanced mutual funds offer a pragmatic path forward, balancing the need for income today and growth for tomorrow. By making informed, goal-oriented choices, you can turn your retirement savings into a reliable source of happiness, comfort, and peace of mind.

Need help creating your personalized retirement fund strategy?

Consult a financial advisor Sagarika Shaw ARN holder with registered mutual funds agency to match fund options with your lifestyle, income requirements, and risk profile.

Why Mutual Funds Outshine Fixed Deposits: A Guide by Sagarika Shaw, Mutual Fund Distributor

As a registered mutual fund distributor, I’ve helped countless individuals and families plan their financial future. One of the most common questions I hear is:

“Should I go with mutual funds or stick to fixed deposits?”

Let’s break it down — and I’ll show you why mutual funds are a smarter choice, especially in today’s inflation-driven economy.

Fixed Deposits vs Mutual Funds: The Core Difference

| Feature | Fixed Deposits (FDs) | Mutual Funds |

|---|---|---|

| Returns | 5% to 7% (pre-tax) | 10% to 15% (historically for equity MFs) |

| Liquidity | Low (penalty on early withdrawal) | High (most are liquid in 1–3 days) |

| Tax Efficiency | Taxable as per slab (up to 30%) | Tax benefits via LTCG, ELSS, indexation |

| Inflation Protection | ❌ No | ✅ Yes (especially equity funds) |

| Growth Potential | ❌ Limited | ✅ High, market-linked |

Let’s Talk Inflation — The Silent Wealth Killer

If your FD is giving 6% interest and the inflation rate is 6.5%, you’re actually losing money in terms of real value.

Real Return = Nominal Return – Inflation Rate

FD: 6% – 6.5% = –0.5% real return

On the other hand, equity mutual funds have historically given 10–15% annualized returns, comfortably beating inflation over the long term.

Example: ₹1 Lakh Over 10 Years

| Investment Type | Average Annual Return | Value After 10 Years |

|---|---|---|

| Fixed Deposit | 6% | ₹1.79 lakhs |

| Mutual Fund | 12% | ₹3.10 lakhs |

That’s a ₹1.31 lakh difference — and it compounds even more over 15–20 years!

Tax Efficiency Matters

FDs are taxed as per your income slab. If you’re in the 30% tax bracket, that 6% FD return becomes only 4.2%.

Mutual funds offer:

- Equity MFs: LTCG taxed at only 10% (above ₹1 lakh gains)

- Debt MFs: Indexation benefit for long-term holding

- ELSS funds: ₹1.5 lakh tax deduction under Section 80C

My Advice: Don’t Let Inflation Erode Your Savings

FDs are safe, but safety shouldn’t mean stagnation. If you want your money to grow, keep pace with inflation, and build real wealth — mutual funds are the way to go.

You can even balance risk by choosing:

- Hybrid Funds (equity + debt)

- Index Funds (broad-market, low cost)

- Systematic Investment Plans (SIP) for disciplined wealth building

Final Word from Sagarika Shaw

As a mutual fund distributor, I don’t just sell funds — I offer financial empowerment. Your future deserves more than just “safe” returns — it deserves smart, inflation-beating growth.

Need a personalized investment plan?

Let’s connect. I’ll help you find the right mix of mutual funds for your goals — whether it’s retirement, children’s education, or wealth creation.